Exploring open finance for product innovation part 1

Open finance is similar to open banking but takes one step further to encompass a broad range of financial data. This open ecosystem can foster...

Embedded finance is meeting consumers in specific contexts, removing barriers and improving customer experience.

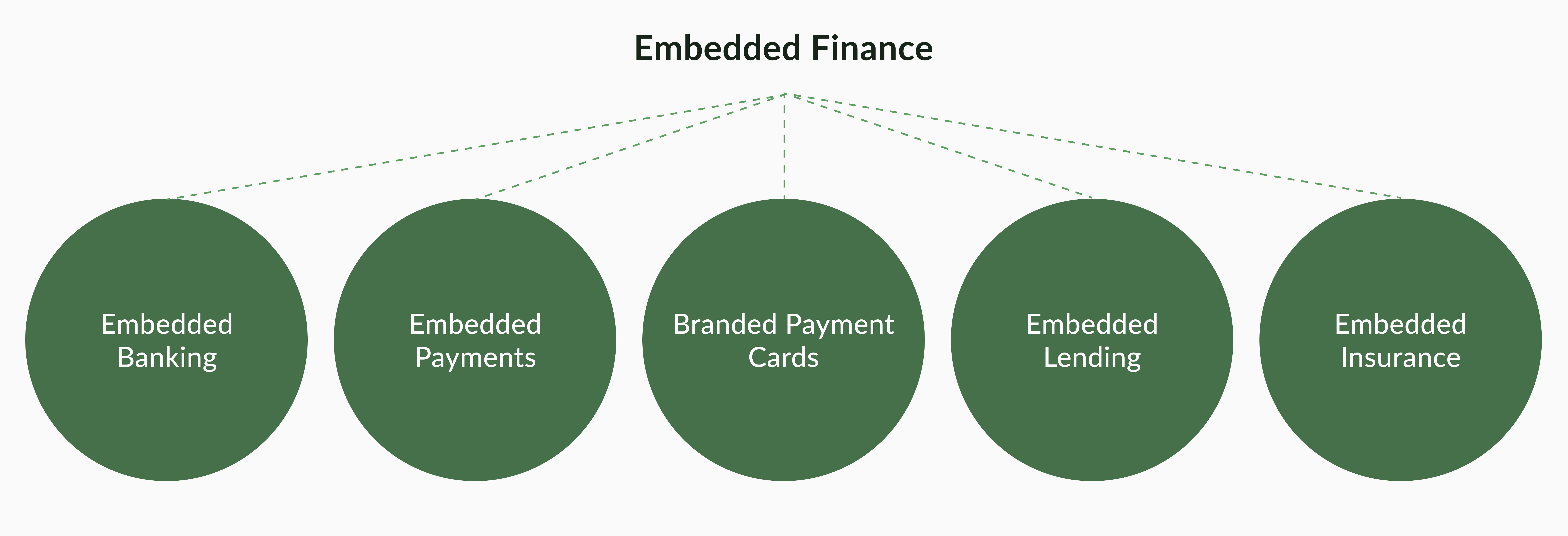

Embedded finance, simply put, is when a non-financial company offers financial products and services through APIs and platforms. Embedded finance allows companies to access and utilize financial services provided by third parties.

This, in itself, is not new - consider that retail stores have offered branded credit cards for years, like Macy’s or Costco. What is new about embedded finance these days is the technological capabilities. Quick and easy integration into easy-to-access digital interfaces, such as apps, digital wallets, rewards programs, insurance, and more is making embedded finance highly attractive to businesses and consumers alike.

There are several specific types of embedded finance:

Embedded finance is increasing in popularity and can be found in multiple industries. Globally, embedded finance is projected to grow at a CAGR of 27.5% from 2022 to 2029, reaching US$200 billion in market value. Here are some prominent examples:

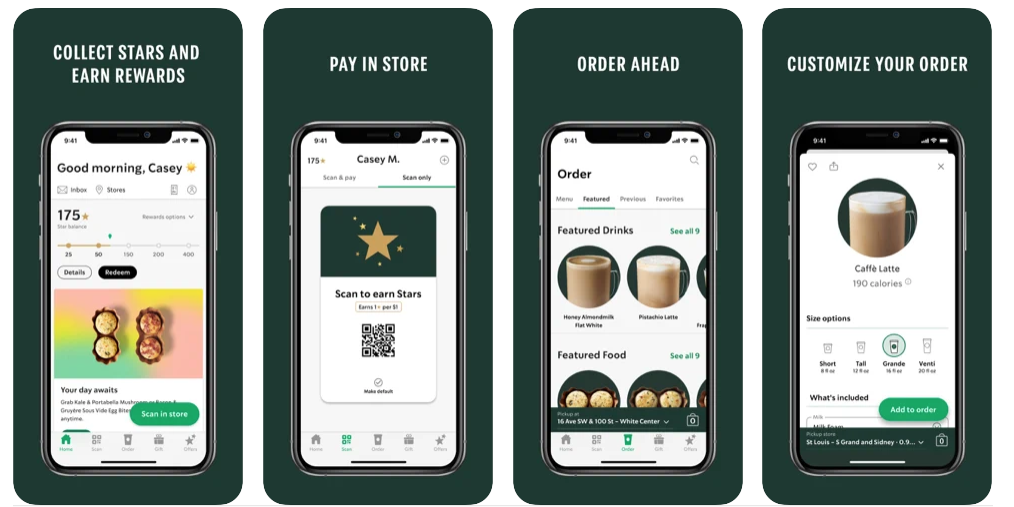

My Starbucks, the Starbucks loyalty app, is a prime example of embedded payments due to its successful in-app mobile payments system.The program rewards customers with “stars” or points that can be redeemed for gifts like complimentary coffee, bakery items and retail merchandise. Every time a customer spends $1 through the app, he/she gains 1 star. If a customer pre-loads money onto the Starbucks app and uses it to pay, he/she gains 2 stars. This incentive has resulted in a US$1.628 billion source of free lending for Starbucks, outperforming 85% of U.S. banks.

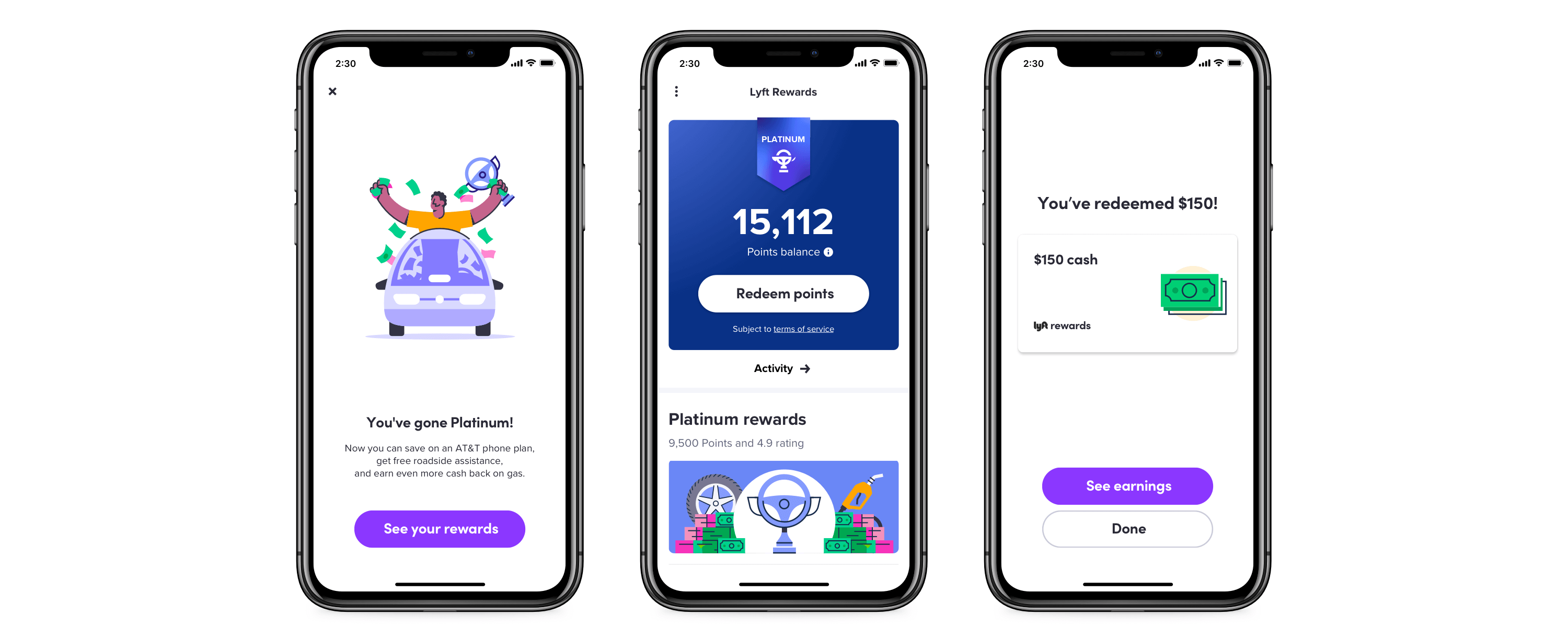

Lyft launched its co-branded debit card with Mastercard in 2019 to give their drivers immediate access to pay after each ride. The card also offers other gig economy benefits, such as 4% cash back on dining, ATM access, identity theft protection, and $0 account fees.

Buy now, pay later (BNPL) is a quickly growing example of embedded lending, projected to be used by 1 in 4 shoppers by 2025. Affirm is a popular BNPL service that allows merchants to provide flexible payment plans for customers without any interest fees. Customers are able to receive their purchases immediately, but spread their payments out over time. Affirm’s technology is easy to integrate into payment processing technology on e-commerce sites, and the service has been shown to benefit merchants through higher average order values and conversion rates.

Embedded finance delivers financial products and services to consumers right at the point of need, removing friction from the consumer journey and increasing purchase completion. Don’t want to spend $200 right now? Spread it out through BNPL! Concerned about travel insurance for that flight ticket? No problem, add it at checkout. Want to round up your daily purchases to help you pay down debt? Do it as you shop day-to-day. Embedded finance is a multi-vertical technology that meets customers in specific contexts, removing barriers and improving understanding.

Embedded finance is quickly becoming a popular offering by non-financial companies to decrease consumer journey friction and increase customer engagement. The rise of open banking and open finance will accelerate this growth.

As an embedded finance platform, Olive delivers open finance services for clients. We expand our capabilities beyond financial data by focusing on outcomes. What kind of outcomes? Simply put, the ones that matter for your customers, and therefore, for your business. Whether it's helping to invest, save, donate or purchase, Olive can power goals.

For more information, check out Olive's use cases. You can also chat with an Olive expert.

Open finance is similar to open banking but takes one step further to encompass a broad range of financial data. This open ecosystem can foster...

Open finance is similar to open banking but takes one step further to encompass a broad range of financial data. This open ecosystem can foster...

Open finance, the secure sharing of financial data, covers more services and has wider impact on consumers compared to open banking.